How to Get a Commercial Loan in Turkey: A Guide for SMEs

The vast majority of SMEs operating within Turkey experience severe difficulties in accessing commercial loans, which is one of the most critical tools to support their financial growth. Although bank loan approval processes in Turkey may seem complex, they are actually systematic evaluations based on specific criteria. In this guide, we explain every step.

Which Financial Ratios Do Banks Look at the Most?

In the loan evaluation process, the first area banks examine is the company's financial ratios. The current ratio, debt-to-equity ratio, and EBITDA margin are at the center of this evaluation.

Particularly when the current ratio drops below 1.5, banks increase their collateral requirements. The EBITDA/Financing expenses ratio is expected to be a minimum of 1.2.

- Current Ratio ≥ 1.5 (short-term debt coverage)

- Debt/Equity ≤ 3 (leverage level)

- EBITDA Margin ≥ 8% (operational profitability)

- Net Profit Margin ≥ 3% (sustainability)

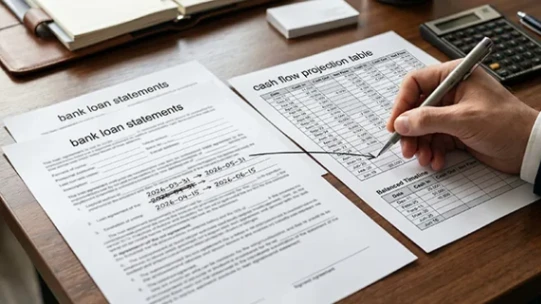

Which Documents Are Required for the Application?

Lack of documentation is one of the most common reasons that both prolongs the loan process and negatively impacts the application. With the correct document package, the process can be reduced to an average of 3 business days.

The basic document package consists of:

- Independent audit report or CPA-approved balance sheet for the last 3 years

- Cash flow projection (12-24 months)

- Appraisal report for the real estate to be shown as collateral

- Articles of association and current signature circular of the company

- Documents showing the partnership structure

Can a Loan Be Obtained Without Collateral?

The answer to this question, which many business owners seek, depends on the conditions. Treasury-backed KGF (Credit Guarantee Fund of Turkey) guarantees pave the way for unsecured or low-collateral loan utilization.

The loan amount a company can utilize with a KGF guarantee can go up to 10 times its equity size. However, to benefit from this opportunity, the company must have an operating history of at least 1 year.

Pre-Application Checklist

- Calculate your financial ratios and compare them with bank threshold values

- Prepare your income statement and balance sheet for the last 3 years

- Update your cash flow projection

- Obtain current appraisal reports for your real estate collaterals

- Query your eligibility for a KGF guarantee

- Verify that you have no outstanding tax or social security (SGK) debts in Turkey

- Clean up your credit history (KKB) or prepare an explanation

- Apply for offers from at least 3 banks and compare them

Frequently Asked Questions

Bir uzman yardımına ne dersiniz ?

18 yılı aşkın deneyimimizle, işletmenize en uygun kredi yapısını ve bankayı belirliyor, başvuru sürecini başından sonuna yönetiyoruz.

Danışmanlık Alın →